The British manufacturing sector has long been braving a storm of surging energy costs, increasing global competition, offshoring, and a hollowing out of our raw materials infrastructure. The new "Vision 2035: Critical Minerals Strategy" (released complementary to the Modern Industrial Strategy and the Defense Industrial Strategy) marks a necessary shift in approach. It finally challenges the dangerous assumption that the global market will always provide the minerals and materials we need to survive.

The strategy makes no illusions that compared to the US and EU, and by virtue of geography, Britain will struggle to fully domesticate raw material extraction. Indeed, the publication of this document is a recognition that meeting our stated ambitions in strategic manufacturing shifts will be challenging when competing with the global market for materials, particularly where the current domestic supply is inadequate. For example, in the case of vehicle electrification, the demand for copper necessary for electric motors is set to double and demand for lithium for batteries will increase elevenfold.

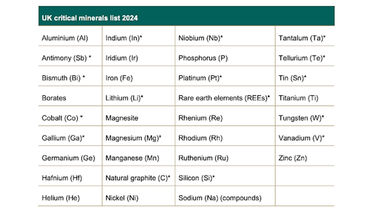

Building on the identification of critical minerals in the 2024 Criticality Assessment by the UK Critical Minerals Intelligence Centre, CMIC, see image below, this strategy further specifies copper, uranium, chromium, beryllium and graphite (natural and synthetic) as “growth minerals” that will benefit from opportunities to streamline environmental and regulatory challenges around domestic production, as well as gaining eligibility to access funding and finance opportunities such as the National Wealth Fund for projects that will improve domestic availability. However, direct access to funding opportunities for projects in critical and growth minerals is limited in this strategy to £50m which sits in stark contrast to commitments such as €3bn in the RESourceEU action plan.

There is a commitment to try and protect new ventures in the critical minerals supply chain from global price volatility in order to bridge the gap between venture investment and operation. This is particularly welcome given the dominance certain market competitors can enjoy in particular mineral classes leading to oversized influence on subsequent supply and demand. This is complemented by a requirement to have no more than 60% of a critical mineral from a single country by 2035.

Other important headline ambitions are to have 10% of UK demand in the aggregate met by domestic refining and extracting, with a specific sub-demand on Lithium production at 50,000t Lithium Carbonate Equivalent; and to have 20% of total annual UK industrial demand for critical minerals met by domestic recycling initiatives.

On energy prices, there is the announcement of specific measures to address the current uncompetitive and deeply unattractive environment for an innovator or manufacturer looking to improve domestic availability of critical or growth minerals. There are the British Industrial Competitive Scheme (BICS) that looks to introduce exemptions from policy costs and network levies such as the Renewables Obligation and Feed-in tariffs, targeting a reduction in energy costs of up to £40/MWh in approximately 7,000 “foundational” manufacturing businesses. This measure is out to consultation immediately with applications set to open in April 2027. The existing British Industry Supercharger (BIS) is set to be updated to increase reliefs of network transmission and distribution charges from 60% to 90%, with an aim to bring British energy-intensive manufacturing prices closer to French and German levels.

The Henry Royce Institute at the University of Sheffield is well-versed in the challenges of critical mineral efficiency. Our world-leading Research and Innovation is driven by the need to secure alternative supply chains and valorise onshore waste streams. This commitment is exemplified by our pioneering 'Designing of Alloys for Resource Efficiency' (DARE) programme and the DSTL-funded ATiTUDE project.

The urgency of the latter work is highlighted by CMIC data, which identifies that 38.7% of the UK’s titanium supply relies on trade with China. Furthermore, secondary sources reveal deep supply chain fragilities; for instance, imports from Germany likely originate from third parties like Russia, which maintains dominance in the global titanium market. To address this, the ATiTUDE programme leveraged Royce’s investment in leading Field Assisted Sintering Technology (FAST). This capability has already demonstrated a fully domestic supply chain, one located within two miles of the Royce Discovery Centre even, that recycles waste titanium swarf into forged products.

These research and development innovations will be key to meeting the strategy's ambitions for 20% of a critical minerals demand will be met from recycling of onshored material. The expert metallurgists and materials scientists that the Henry Royce Institute network brings together form a key resource for innovators in the extraction and refinement supply chain to draw upon, with players such as the Materials Processing Institute currently building capability in both primary and secondary materials recovery and midstream processing and recycling, or the ReMake Value Retention Centre at the National Manufacturing Institute of Scotland seeking to build material resilience for nationally important manufacturing capabilities.

What remains to be seen is if the strategy will manage to deliver the promised benefits to onshoring and recycling efforts without a realistic approach to industrial energy costs in the critical minerals supply chain. Reliefs can be offered to energy intensive industries, but these do not affect the underlying problem of high wholesale prices, and with the BICS set to be rolled out in 2027 (after a fifth of the time period covered by the strategy) this does not provide interim support to those who would want to implement innovations and investment now that would deliver in time for 2035. At time of press, Britain had the highest industrial energy prices in the world - c.3-4x the likes of the US, Russia, China, France. The manifestation of current energy policy and pricing interventions in the market has still resulted in government intervention to prevent the collapse of strategically critical manufacturing and minerals sites such as Sheffield Forgemasters, British Steel and recently Ineos Grangemouth.. We wait with hope that the strategy’s promised support and financial incentivisation will bring about desired returns in the face of such conditions.

Similarly, while overtures to improved regulatory and environmental assessments are welcome as well as a promise to fast-track these for growth minerals, we encourage bold strategic thinking to ensure these are successfully streamlined through to processing stages, including in the face of potential political opposition. In comparison, RESourceEU mandates projects of strategic importance can be defined as being of overriding public interest and must be prioritised by law. It also introduces legally binding caps on the total duration of the permit-granting process to avoid extended and potentially dilatory bureaucratic review.

We also encourage further appraisal of critical and growth mineral demand signals based on a whole government approach - for example, while predicted demands for electrification related minerals are fully embedded in a context that considers DfT requirements in phasing out of Internal Combustion Engine vehicles, a transition to a clean energy landscape that includes nuclear fusion reactors such as Spherical Tokamak Energy Production in West Burton (and plans for further reactors beyond 2035) would require even more demand on lithium and tungsten than currently included in forecasts.

In summary, we are excited to contribute to an ambitious policy programme of onshoring and improving the resilience of our critical minerals supply for industries such as defence and clean energy. While there is room for improvement in the baseline support of such a strategy, having a clear destination focuses research initiatives and decision making for both funding bodies and private capital.

For innovators interested in exploring recycling technologies, whatever the material or mineral, please get in touch via royce@sheffield.ac.uk or on our LinkedIn platform to continue the conversation.